How to Identify Your Retirement Income Beliefs

How to Identify Your Retirement Income Beliefs

The Development of RISA®

Retirement income planning is a relatively new field in the financial advisory profession. Traditionally, wealth management was dedicated to accumulating assets before retirement. No thought was given to the differences that may occur after you retire. If anything, retirees were simply told to withdraw 4% of their assets during the first year of retirement, then adjust the amount for inflation every year thereafter. But that wasn’t exactly a retirement income strategy; it was a withdrawal strategy. Moreover, the old “4% rule” was based on assumptions that are now outdated.

What got you here won’t get you much farther

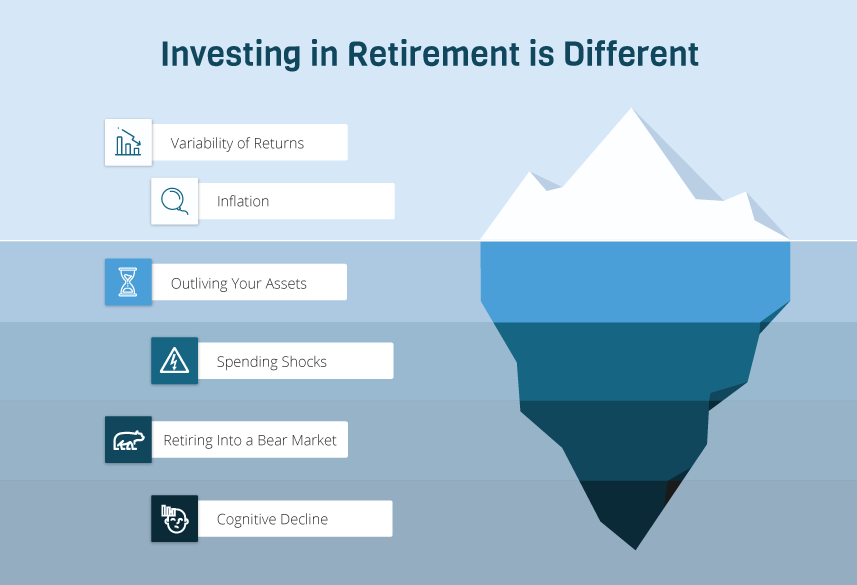

The old way never addressed how to manage your portfolio in retirement. Investing in retirement is different. In addition, nowadays there is less reliance on traditional risk pooling tools such as defined-benefit pensions. Retirees are living longer than ever, too, and many of them face unexpected healthcare and long-term care expenses that outpace inflation.

In retirement, your financial needs, desires, goals, strategies, and approach may shift from what they were before. You might become more concerned about sustaining enough income to support your spending needs for the rest of your life, less concerned about growing your nest egg or maximizing returns. You might think more about your legacy or how much you’re leaving for your grandchildren or favorite charity, while still supporting your standard of living and maintaining sufficient liquidity in case of unexpected expenses. Or something else entirely.

Naturally, retirees must find a way to use their financial resources to support themselves for the remainder of their lives—ever mindful of market volatility and interest-rate risks. But exactly how you prefer to go about achieving those goals is unique to you, and it might look different once you’re retired.

How to Retire with a Smile

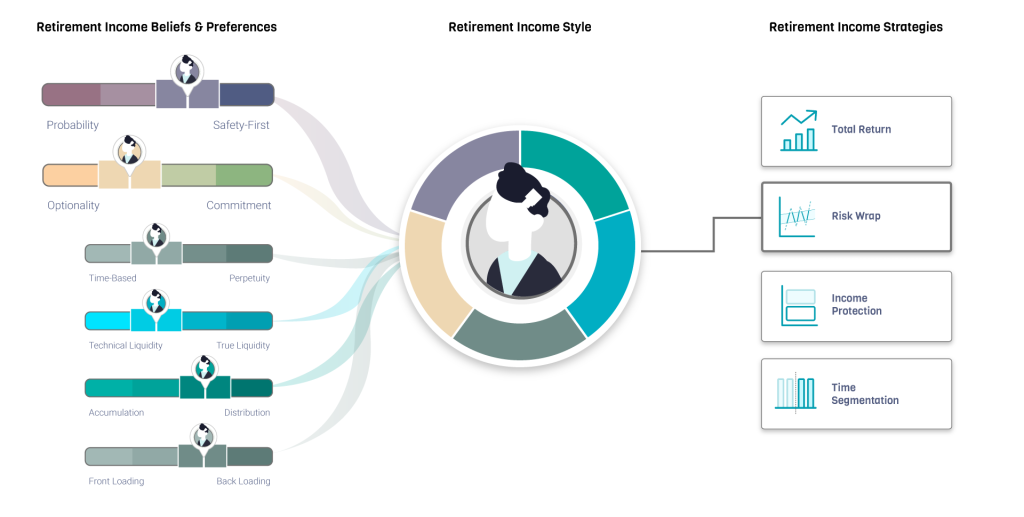

Our Retirement Income Style Awareness (RISA®) tool is designed to capture the multifaceted aspects of a retirement income plan beyond a traditional accumulation-focused portfolio guided by a minimal risk tolerance questionnaire.

The RISA® system is designed to match a variety of preferences about how you’d like to source your retirement income, which hasn’t been done before. It translates your specific preferences into a snapshot of appropriate, viable approaches that fit your style. The process is a little like when you chose a career. You needed to decide how you wanted to draw a paycheck. Some people prefer the reliable income and pension of a civil service job, while others opt for a more fluctuating income stream that has the potential for greater total income in the end. Some favor a long-term contract with a steady paycheck, others like the flexibility of being an independent contractor who chooses his or her own hours and projects.

Similarly, the RISA® helps guide you to retirement-income strategies that fit your style. It’s an empowerment tool. After all, no single approach or product works for everyone. Our methodology effectively identifies your personal preferences and matches them to specific retirement income strategies and recommendations for you to choose.

Why this is important

The concept is important for all retirees. It’s constructed to help them not only achieve their goals but feel confident in their retirement plans. Recognizing the presence of different financial styles means acknowledging that different retirement income strategies are and are not appropriate for specific individuals. Defining personal preferences and matching them to a specific recommended strategy is an essential step toward ensuring that you and your retirement income plan are aligned. Failing to address personal preferences, however, can lead to strategies that aren’t properly implemented or followed. This, in turn, can lead to costly and constant revisions of your retirement plan that are bound to fail.

Even if you’re working with an advisor, this assessment can be valuable. Advisors achieve better outcomes if they’re armed with appropriate knowledge. Most advisors only offer what they know best or what they feel most comfortable with, or are otherwise licensed or incentivized to provide, with little consideration for a client’s deep-seated preferences and comfort levels. Let’s face it: There’s little point in spending time describing an annuity, say, if a client has little interest in that option.

Our system ensures that your chances of attaining better overall outcomes and enjoyment of your retirement will improve—because it’s designed to give clarity and instill confidence in your retirement income plan.

How This Works

All this may sound like a tall order. But we’ve designed a plain-language questionnaire that automatically assesses your primary RISA® Profile. The Profile can help you and/or your advisor zero in on how you’ll be most comfortable (and most likely to succeed) sourcing your retirement income.

Personal styles are nuanced, multifaceted, and multilayered, of course. Our research has broken down retirement income styles into specific factors. Expressed as a range of choices, the questionnaire examines each of these factors to gauge your individual preferences related to financial decision-making. Rating a variety of real-world scenarios on a scale of 1 to 6, you will help us identify the complexities of your retirement wishes and biases.

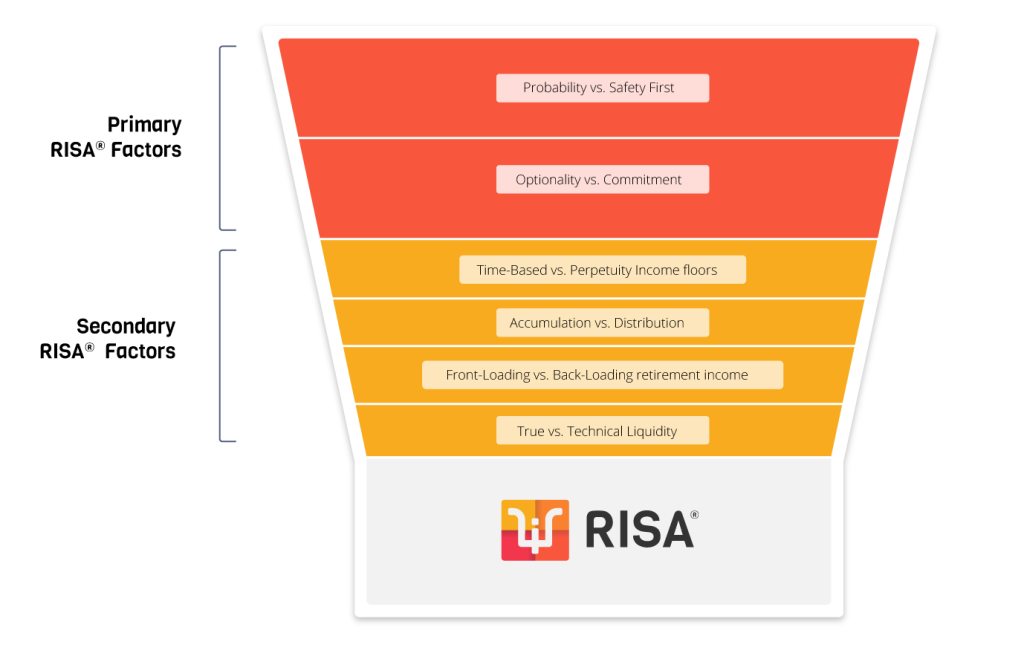

Your RISA® Profile is derived from where your responses land on two primary dimensions. They are:

- Probability-Based vs. Safety First (PS)

- Optionality vs. Commitment (OC)

Probability-Based vs. Safety-First (PS)

Probability-Based vs. Safety-First (PS) details exactly how individuals would like to source their retirement income. Probability-Based income sources are dependent on the potential for market growth to provide a continuous and sustainable retirement income stream. This includes a traditional diversified investment portfolio or other assets that have the expectation of growth. On the other hand, Safety-First income sources incorporate contractual obligations. The income provided by these sources is less exposed to market swings. A Safety-First approach may include protected sources of income such as defined-benefit pensions, annuities with lifetime income protections, or government bonds held to maturity. The Safety-First approach does not depend on an expectation of market growth.

Though no strategy is completely safe, the inclusion of contractual protections implies a relative degree of safety compared to unknown market outcomes. With pensions and annuities, income is further supported through what are called mortality credits or mortality pooling. That’s an actuarial term that relates to life expectancy. It can reduce the cost of income guarantees.

Optionality vs. Commitment (OC)

Optionality vs. Commitment (OC) delves into the degree of flexibility sought. Optionality reflects a preference for keeping options open, a desire to maintain flexibility in order to respond to economic developments or changing personal situations. This preference aligns with retirement solutions that do not have pre-determined holding periods and are easily adjusted. Conversely, Commitment reflects a preference for committing to one solution. That generally means you’re less concerned about unfavorable economic or personal developments, confident that your strategy solves for such contingencies. The security of having a dedicated retirement income solution outweighs missing out on potentially more positive future outcomes, and it may provide further satisfaction from having made decisions and not feeling a lingering sense that the decision is hanging over you on your to-do list. There can also be satisfaction from planning in advance and not leaving difficult decisions for later, when your ability to make decisions may be hampered by stress or cognitive decline.

Four Secondary Factors

In addition, we developed four secondary factors to provide further refinement of your RISA® Profile recommendations:

- Time-Based vs. Perpetuity Income floors (TP)

- Accumulation vs. Distribution (AD)

- Front-Loading vs. Back-Loading retirement income (FB)

- True vs. Technical Liquidity (TT)

Time-Based vs. Perpetuity (TP)

Time-Based vs. Perpetuity (TP) refers to two different income planning approaches. Time-Based funding strategies are used to fund fixed windows of time in retirement. But other people prefer to fund an income floor that lasts in perpetuity. The latter involves using lifetime income protections through insurance or annuity risk pooling.

Accumulation vs. Distribution (AD)

Accumulation vs. Distribution (AD) is the difference between concentrating on portfolio growth (i.e., accumulation) while retired, even though it may entail a bumpier income stream, or focusing on maintaining a more predictable income (distribution) even if that means not leaving the biggest amount possible at death. Those with an Accumulation mindset will be more comfortable building a retirement portfolio using the tools of Modern Portfolio Theory, which is the traditional mathematically balanced framework for building a portfolio with an expected return that’s maximized for a particular level of risk. On the other hand, those with a Distribution mindset prefer to optimize portfolio distributions and income, with less concern for maximizing the overall return.

Front-Loading vs. Back-Loading Income (FB)

Front-Loading vs. Back-Loading Income (FB) relates to the amount and pace of income you receive throughout retirement. Do you feel more comfortable Front-Loading portfolio distributions to better ensure that savings can be enjoyed during the early stages of retirement, when you’re more likely to be healthy and active? Or would you prefer spending less in early retirement years, to better ensure you won’t need to make cuts during the later stages of what could be a very long retirement? If you expect to spend more money enjoying your early retirement years, you probably favor Front-Loading Income. But if you fear outliving your assets, you have what’s called a “longevity risk aversion,” meaning you’d prefer Back-Loading Income and being more conservative with distributions in early retirement.

True vs. Technical Liquidity (TT)

The final factor, True vs. Technical Liquidity (TT), relates to two different financial planning definitions of liquidity. Those who prefer True Liquidity would like to have assets earmarked as reserves for future unexpected events that can derail a retirement plan. To be truly liquid, assets must not already be designated for other financial purposes such as planned retirement expenses or specific legacy goals. True Liquidity can involve the use of cash set-asides, buffer assets, and insurance. Those who prefer Technical Liquidity, however, would rather raise cash for unexpected expenses from assets that are earmarked for other goals, as necessary—with an understanding that cuts may then need to be made elsewhere. If you’re comfortable with Technical Liquidity, you may be fine with fewer assets in your retirement income plan; you don’t find it necessary to hold as much in reserve as a cushion for emergencies.

Does the RISA® work?

In our research, the two main RISA® factors, Probability-Based vs. Safety-First (PS) and Optionality vs. Commitment (OC), were shown to successfully identify participants’ retirement income styles and provide statistically significant insights into the types of retirement risks they were most concerned about. In addition, the RISA® was significantly telling about how they felt about the various secondary retirement income factors detailed above. Our paper, “A Model Approach to Selecting a Personalized Retirement Income Strategy,” provides a detailed review of our findings.

What this means

The RISA® is the first tool to capture the multidimensional aspects of a retirement income plan. Because the RISA® showed both reliability and validity, that means we now have a multidimensional tool that has been shown to do a better job of identifying …

- Retirement Concerns

- Retirement Income Styles

- Preferred and Appropriate Retirement Incomes Sources

Conclusions

For those who have been saving and accumulating in anticipation of future retirement, the question of what to do with the accumulated assets upon reaching retirement has always been a problem. Retirees are becoming more responsible for figuring out how to save, invest, and then convert their savings into sustainable income for an ever-lengthening number of retirement years. But at present, the guidance and strategies provided to them are largely dependent on the viewpoints of a few so-called pundits.

Now, however, there is a new way to find how best to transition to retirement, in a custom-tailored manner that works for you. In much the same way you chose a career to fund your accumulation years, based on your interests, you can now fund your retirement years based on your unique set of preferences.

Next steps

You can take these scores and explore strategies that are tied to your RISA® style. The RISA® factors present a significant leap ahead in retirement income planning and lay a foundation for achieving better retirement outcomes. Moreover, you can effectively quantify various retirement income styles and create reliable measures around them.

Once your RISA® Profile is identified, you will quickly and manageably have a range of strategies presented that “feel right.” The RISA® provides an effective framework for determining individual retirement income preferences and relevant solutions. It generates a RISA® Matrix, made up of quadrants that can help position the retirement income strategies that match your choices. With that framework, you are equipped to search for a strategy that complements it. You are in control, empowered.

Take the RISA® and see how it specifically points out strategies that fit your profile.