A protected retirement income strategy that is untethered to stock market volatility.

A Bird in the Hand.

Introduction

Finding and implementing the right strategy for sourcing your retirement income can be a daunting task. A myriad approaches and options are available, and truthfully, many of them will probably work all right, more or less, at least for a time. But which approach is best for you—is most precisely suited to your strengths and weaknesses, your concerns and biases and priorities, your preferences and lifestyle—may be something else altogether. A strategy that’s custom tailored not just to your requirements but to your personality is one you’ll feel good about and, consequently, one you’re most likely to implement with relative ease. It’s the one you’ll be able to stick with because it feels right—and therefore, the one that’s most likely to succeed.

RISA-In-The-Retirement-Process

Our Retirement Income Style Awareness (RISA®) tool can help you identify that solution. From your unique profile, it will show you a range of appropriate options so you can choose what’s best for you. That’s because it’s designed to capture the multifaceted aspects of a retirement income plan beyond a traditional accumulation-focused portfolio guided by a minimal risk-tolerance questionnaire.

RISA® is Different

Unlike any retirement planning tool that’s come before, the RISA® was specifically built to measure a variety of choices about how you’re most comfortable sourcing your retirement income. It translates your choices into a snapshot of appropriate, viable strategies that fit your style. It’s an empowerment tool to help you find what’s best for you. No single approach or product will work for everyone, of course. So our methodology effectively identifies your particular preferences and matches them to specific retirement income strategies and recommendations for you to choose. In this way, the RISA® solves the problem of scattershot retirement planning.

Through a series of user-friendly questions, it zeroes in on your unique profile to generate custom-tailored retirement income solutions. The secret behind the system is we’ve broken down retirement income styles into specific dimensions that gauge your preferences in relation to financial decision-making.

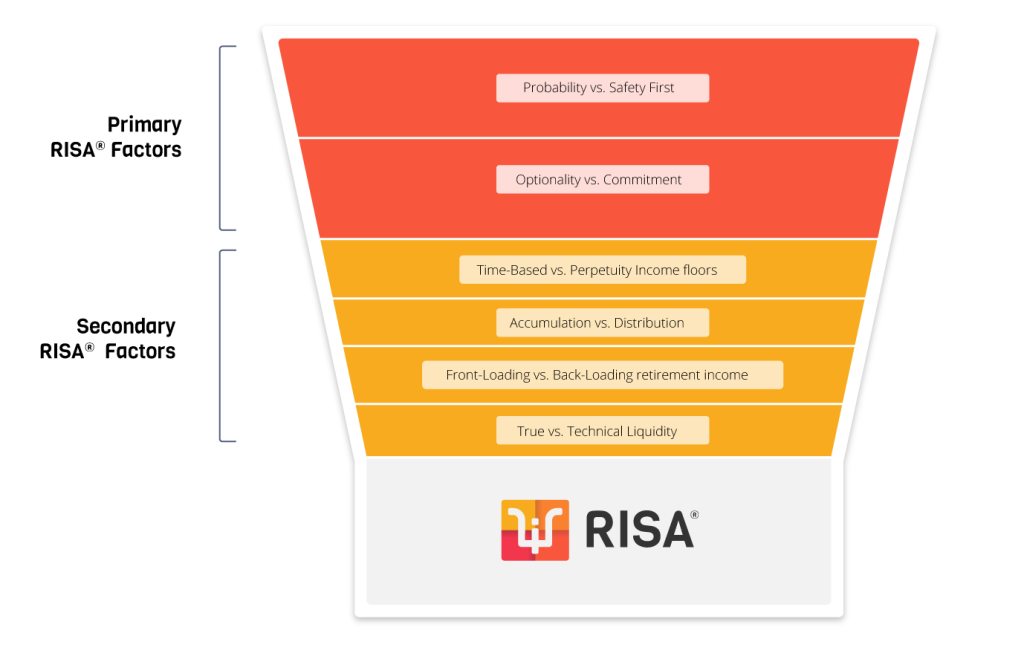

Two Primary Factors

The two primary factors our questions assess are Probability versus Safety First and Optionality versus Commitment. Probability versus Safety First details how you would like to source your retirement income—from sources dependent on potential market growth or from contractual obligations. Optionality versus Commitment delves into the degree of flexibility sought. Maybe you like to keep your options open, or your prefer to commit to one solution and be done. There are no right or wrong answers here. It’s all a matter of preference.

Four Secondary Factors

We then examine four secondary factors to sharpen and refine your profile: Accumulation versus Distribution, Technical Liquidity versus True Liquidity, Front-Loading versus Back-Loading, and Time-Based versus Perpetuity planning. These dig deeper into precisely which type of approach for sourcing retirement income feels best and most fitting for you.

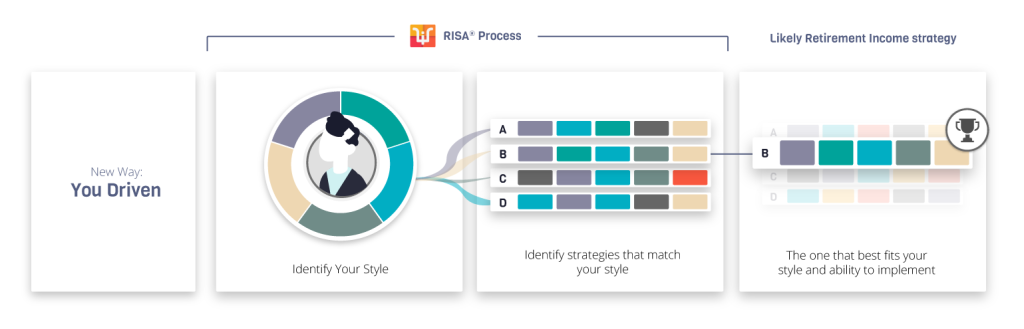

The RISA® Matrix

From there, with this foundation of distinct factors to identify your preferences, we define your RISA® Matrix, which is made up of appropriate and practical retirement income approaches. More specifically, the Matrix lays out four quadrants to delineate your individualized retirement income profile.

Next, we identify the four main strategies that match up with the four RISA® Matrix quadrants.

The Case Study

To illustrate this process, here is an example of how you can identify a retirement income approach that best fits unique personalities and preferences. Your story may be completely different. This is just sample a case study to demonstrate the effectiveness of our system. No one situation or solution is better than the others. You may or may not identify with this case, but that’s okay. What’s best for you depends entirely on who you are.

That, after all, is the point. The retirement income sourcing strategy that’s best for you is one that’s matched to your specific and unique style and preferences.

Suzy and Ray

A bird in the hand… A protected retirement income strategy that is untethered to stock market volatility.

During their working years, Suzy and Ray experienced significant bull markets. But they were children of Depression Era parents and carried a cautious, penny-pinching mindset throughout their lives. They also had friends who lost significant retirement savings in speculative investments. Their consistent focus on securing an income stream, keeping ready access to cash for emergencies, maintaining disciplined savings habits, and indulging only minimal use of debt helped them avoid fiscal landmines as they raised their family. But now they’re nearing retirement—sooner than they’d wished for.

In retrospect, they regret not choosing jobs with pensions that would support them in retirement. Instead, they maximized their 401(k) contributions, blithely expecting to revisit their retirement income situation once they retired. But now what? They understand the logic behind drawing a sustainable income stream from an investment portfolio, but their life experiences have guided them toward preferring a perpetual income floor for essential expenses. Contractually driven retirement income would unchain them from depending on potentially volatile investments, and this degree of independence is terribly appealing to them. Just as they’ve seen friends’ retirements go south from speculative investments, they’ve also seen other friends with a government pension retire happily, never worrying about market volatility. They envy that kind of easy retirement life.

Attaining contractual retirement income appeals to Suzy and Ray for other reasons, too. First, removing market dependence from their basic retirement income needs would free up previously allocated investment capital and enable them to establish an emergency account for unforeseen expenses. So even if they suffer a string of poor market returns, they can adjust their discretionary spending—which is supported by their investment portfolio—without sacrificing their standard of living, if that portion is supported by the contractual income source. Second, because of their good family health history, they expect to live a long life, and the promise of automatic, guaranteed lifetime retirement income that can’t be outlived sounds very attractive. By having an income floor in perpetuity, Suzy and Ray won’t have to revisit how to pay for essential needs every few years.

RISA® Interpretation

Using the RISA® questionnaire, we were able to glean and measure many of the preferences that Suzy and Ray exhibited during their accumulation years as they readied for retirement.

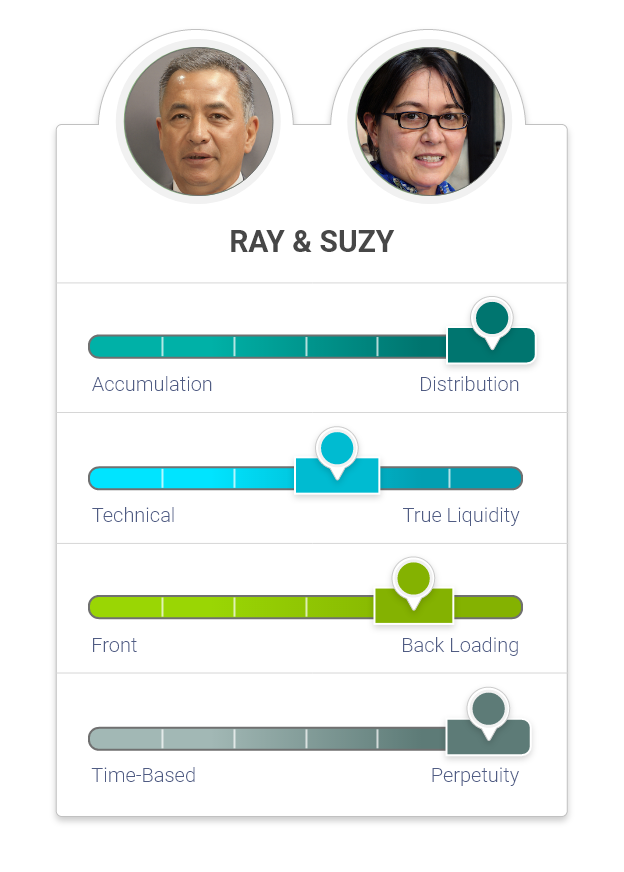

Their RISA® profile looks like this:

Suzy and Ray’s RISA® score reflected many of the preferences that they displayed throughout their accumulation years. It indicates a preference for drawing income from contractual obligations that are less exposed to market swings and don’t depend on market growth—such as defined-benefit pensions, government bonds, or annuities with lifetime income projections. In addition, they are willing to commit to a lasting solution as long as it resolves their lifetime income needs.

In Suzy and Ray’s RISA® profile, the two primary factors were as follows:

Further supporting this view, their secondary factors were:

Their secondary RISA® factors exhibit an emphasis on maintaining a predictable income stream, even if that means not leaving the biggest estate possible for their heirs. The secondary factors also indicate a preference for having certain assets earmarked as reserves for unexpected events, and a desire to backload their retirement because of the fear of outliving assets. In general, they favor being more conservative with distributions in early retirement so there’s enough later to keep them from outliving their assets and becoming a burden to others. Finally, they wish to address potential funding gaps by creating an income floor that lasts in perpetuity.

These preferences reflect a protected income approach that allows for immediate and deferred annuitization. This would support downside spending protection, since it relies on contractually guaranteed lifetime income. With the RISA® in hand, Suzy and Ray can quickly assemble a retirement income plan focusing on the factors they care about most. Maybe now their friends will be envious of them.

Conclusion

While this case study may not match your situation, the RISA® is specifically designed to capture your unique set of biases, leanings, and preferences. It’s a tested and effective custom-tailored tool for an age-old problem: how to structure a retirement income sourcing strategy that feels right and will go the distance.

Financial experts are full of ideas and approaches to retirement income planning, many of which are valid. But they are not based on this kind of detailed assessment of your particular personality and financial style. Our RISA® system solves the problem of cookie-cutter methods by weighing specific measures of how you want to source your retirement income. As in the case described above, the RISA® will generate an appropriate matrix that matches suitable and available retirement income strategies to your particular quirks and desires.

Once you’re armed with this information, you will become a more informed consumer. You will be empowered to choose the right retirement income strategy for you—one that fits as comfortably as an old pair of jeans, one that will feel right for the length of your retirement. That’s important for not just your retirement satisfaction but your ability to stick with the plan. You can’t be expected to implement a strategy that just doesn’t feel right. That’s a recipe for disaster. But with the RISA® assessment, you can feel certain of finding the ideal approach for your situation and personality. That’s one you’ll be able to implement with confidence and ease. As such, it’s the retirement income sourcing plan that’s most likely to succeed for the long haul.

RISA-How-The-RISA-Works

So take our RISA® questionnaire today. It’s easy, and you might even find it fun. But the most important reason to do it now, without delay, is that it could change the course of your retirement. It could improve your odds of successfully maintaining a retirement income strategy in a way you’ll feel good about and enable you to implement it with success.