Once you know your strategy, you need to know how best to implement it.

How to Determine Your Retirement Income Implementation Option

You’ve taken a great first step towards your retirement plan when you identify your own unique retirement income style. This means you’ve zeroed in on your retirement income preferences, which can be mapped to practical, appropriate strategies. These personal views are key to retirement income success. But even the best laid plan will be worthless if it isn’t implemented correctly.

You also need to figure out what implementation method aligns best with your personality and preferences. Any implementation that isn’t correctly aligned with your unique makeup is pretty much doomed to failure. You won’t follow through. You won’t want to. It won’t feel right. It’s like a bad relationship.

Speaking of relationships, you don’t want to work with an advisor who has a different philosophy or approach from yours, who doesn’t work well with what you need. You don’t want someone who might overwhelm you with questions and information that leaves you feeling bogged down and confused. You don’t want someone that seeks your input on most decisions; you just want to enjoy your retirement and have someone else take care of everything. On the flip side, you may not want an advisor that doesn’t involve you enough or doesn’t truly value your feedback on how you want to approach things. Either way, and many others in between, it’s a bad fit. You won’t be inclined to trust or follow the advisor’s suggestions. And frankly, there’s no point seeking expert advice that’s never implemented.

How to ruin your retirement

Such situations could not only ruin your enjoyment of retirement but upend your plans for securing and maintaining retirement income. If you don’t get the implementation phase right, you won’t be able to follow your plan. You’ll end up continually searching for a better way.

You may also feel more comfortable just implementing your plan yourself. With the increasing popularity of, self-directed methods and models for implementing a retirement income plan, such as so-called robo-advisors and other automated investment tools, these options are readily available. However, it’s also easy to shoot yourself in the foot. This is why it’s vitally important to match your financial implementation approach with appropriate methods.

Here’s our one-of-a-kind solution.

The Financial Implementation Matrix

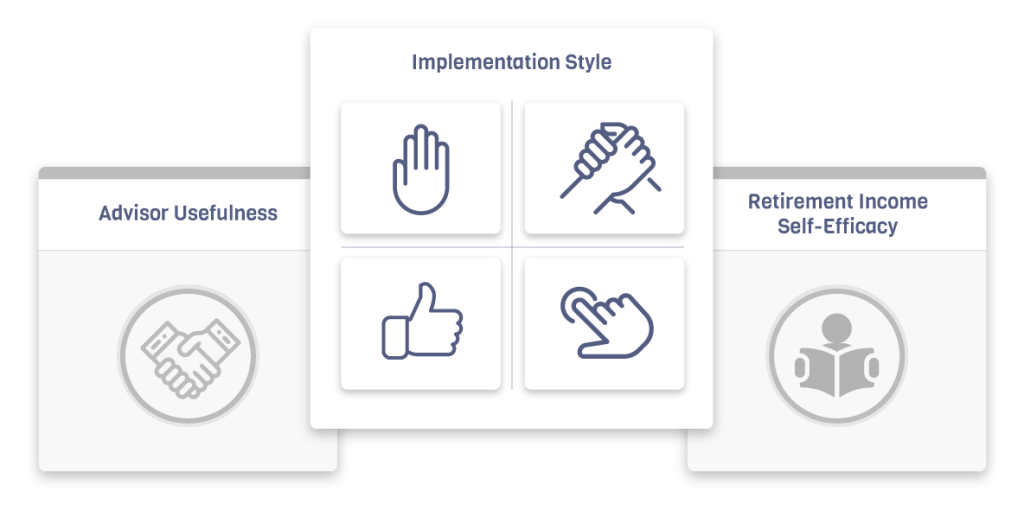

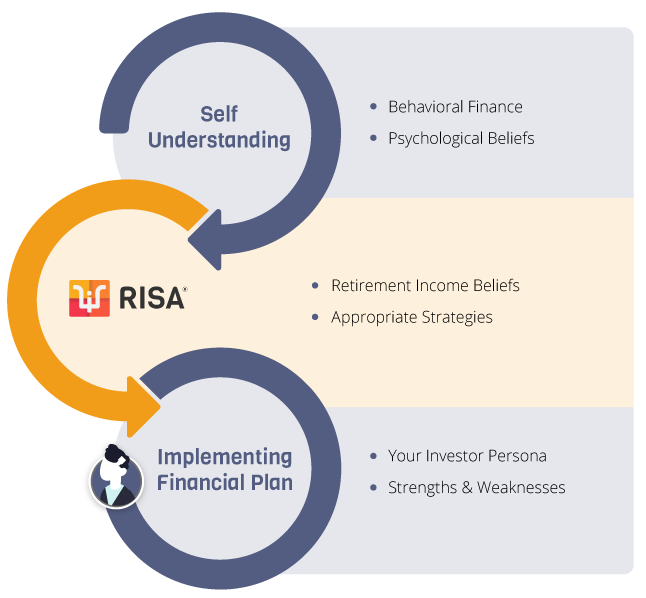

As part of our RISA® project, we created a Financial Implementation Matrix™ that weighs your feelings about different implementation approaches. It helps you identify your particular financial implementation style and how you prefer to implement financial tasks—useful for you and for any advisors you may happen to hire.

The matrix is built on two key measures: “advisor usefulness” and “retirement income self-efficacy.” What follows are summary findings from our research paper, Retirement Income Beliefs and Financial Advice Seeking Behaviors.

Advisor usefulness

Advisor usefulness refers to how you view professional financial help. Various studies indicate the additive benefits that a financial professional can give to overall portfolio returns, but many people continue to believe that advisors aren’t reliable or cost-effective. Mistrust of financial advisors may lead to an underutilization of a valuable resource. Your feelings about advisors make a powerful predictor of whether or not you’re likely to seek and follow an advisor’s help. In fact, this measure alone is more indicative than any other psychological variable. It’s a more powerful factor in the decision of whether or not to use an advisor than age, marital status, net worth, or other demographic variables. A higher perceived usefulness of an advisor means you’re more likely to engage in such a relationship. Perceived advisor usefulness is the key indicator of advisor utilization.

Being able to reliably identify who is most likely to implement a retirement income plan with the aid of a financial advisor is a significant step toward mapping an effective implementation strategy. Instead of trying to convince skeptics of the value of using an advisor, it’s better to identify their reasons—and perhaps provide avenues that maximize how they prefer to receive financial information. By facilitating this approach, individuals may be more likely to engage in behaviors that ultimately lead to retirement income success.

Retirement income self-efficacy

The retirement income self-efficacy scale measures your degree of confidence in your own understanding of how to assemble and implement a retirement income plan—your assessment of your own skills. It’s connected to the conviction of how well you can successfully execute a specific course of action. This differs from general self-confidence because it represents your perception of competency, of being adept at achieving specific goals. It may, in fact, indicate overconfidence. After all, you can be good at saving money, say, but not a very smart investor; just because you’re skilled at one doesn’t mean you’re equally adroit at the other. Along with this overinflated sense of self-efficacy can come a negative view of the usefulness of financial advisors. So measuring your degree of financial self-efficacy is another important construct to implementing retirement income strategies.

Our investigation found retirement income self-efficacy is strongly associated with several retirement-related concerns. First, it correlates with a high degree of worry about being able to maintain a certain lifestyle. Second, it’s negatively associated with fears of outliving your income, known as longevity risk, and fears of not having sufficient funds readily available for unplanned emergencies, also known as liquidity risk. Yet a high degree of self-efficacy also connotes a high degree of nest egg satisfaction—i.e., feeling that your retirement is on track with your expectations—and a low degree of retirement anxiety, or low levels of comfort with your retirement income strategy.

By graphing where your preferences and tendencies land on these two scales—advisor usefulness and retirement income self-efficacy—we can identify four distinct investor personas, each of which can be aligned with certain financial implementation approaches. Besides helping you figure out your persona, and which retirement income implementation approach works best for you, the matrix also provides advisors with insights into the type of financial service model each persona may best identify with.

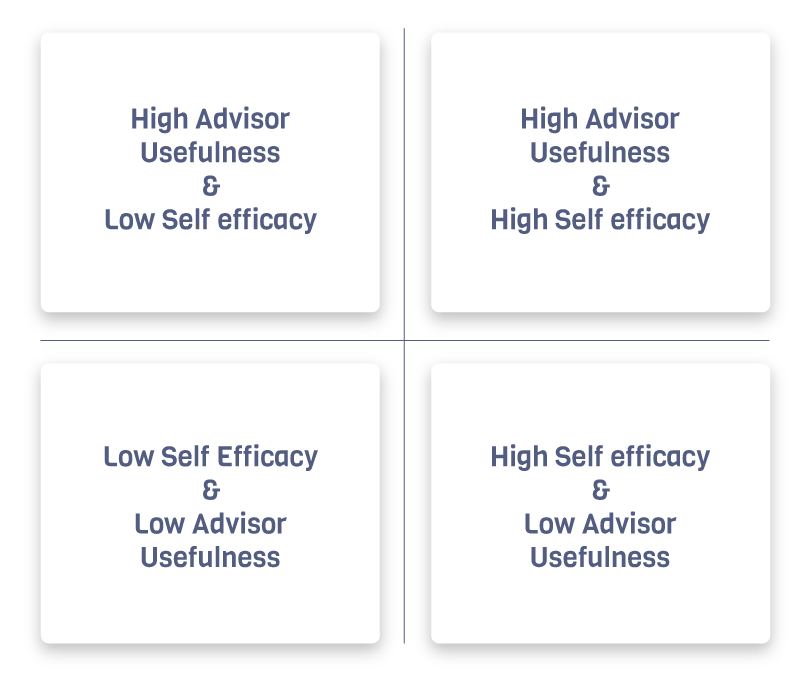

The four personas are:

- The Delegator

- The Collaborator

- The Self-Directed Investor

- The Validator

The Delegator

As demonstrated in Figure 1, the top left quadrant identifies someone who is below average on perceived financial self-efficacy and high on perceived advisor usefulness. As a result, this person is more likely to have an advisor take the lead role in guiding her or his retirement plan. A profile score in this quadrant would be indicative of a “delegator persona.”

Delegators tend to exhibit a high degree of concern about longevity, significant anxiety about their retirement income strategy, and financial biases. These problems may be why they’re often willing to outsource financial tasks to professionals, which is probably a good thing. Advisors can help them address their concerns and biases. They can address specific themes and events that put the clients’ fears in perspective and reveal the clients’ biases. Advisors can build a financial plan around these shortcomings, one that focuses on specific goals to achieve retirement income success.

The Collaborator

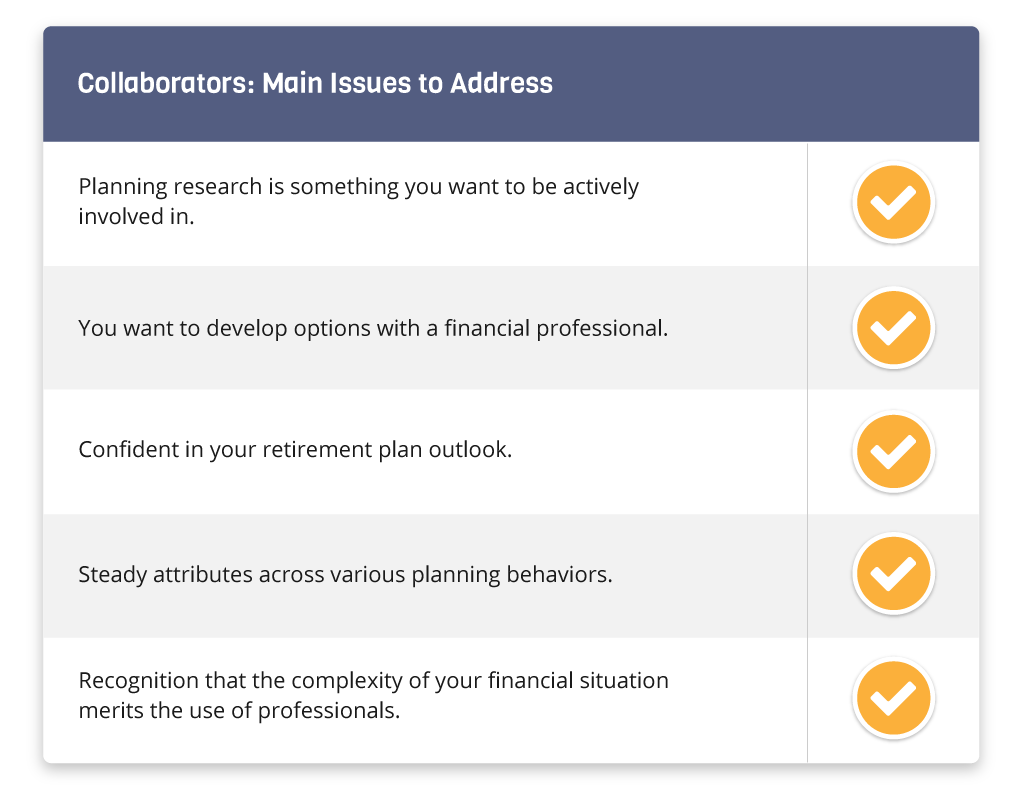

The top right quadrant identifies someone who is high on both self-efficacy and advisor usefulness. This describes a person who feels very confident about her or his own ability but also appreciates the value of an advisor. This type of personality usually enjoys contributing as an active partner with a financial professional, not as a passive recipient of recommendations. A profile score in this quadrant indicates a “collaborator persona.”

Collaborators don’t exhibit significantly high or low levels of retirement income concern, financial biases, financial literacy (sometimes called numeracy, or the ability to comprehend certain mathematical concepts but not others, such as the impact of portfolio volatility), or inertia (not moving forward or following through on financial plans in a timely manner). They are pretty steady people who tend to have a high net worth. They realize the complexities that can arise from having wealth, which may lead them to collaborate with advisors. While a delegator can appreciate an advisor’s taking the lead, a collaborator may prefer situations that allow for active input in developing and implementing a retirement income strategy. So more advanced levels of communication would be appropriate. For these clients, advisors should expect to provide sound reasoning behind every decision. They need to answer not just what? but why?

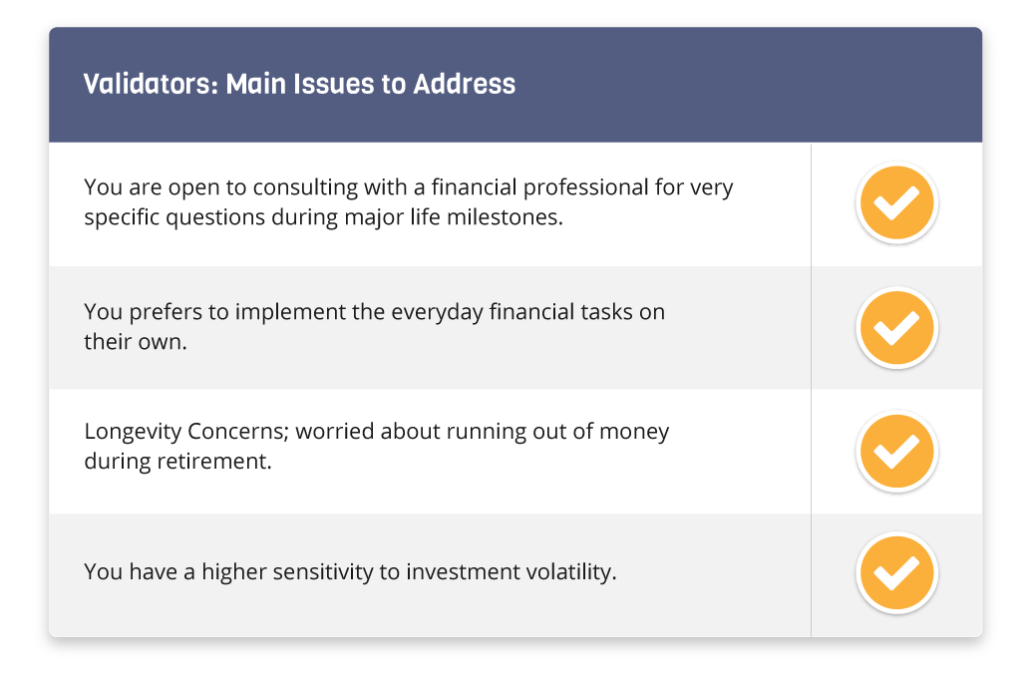

The Validator

Finally, the bottom left quadrant identifies those who are below average on perceived financial self-efficacy and low on perceived advisor usefulness. While they don’t value an ongoing advisory relationship, their low self-efficacy scores leave open the possibility of seeking specialized guidance for particularly difficult financial decisions or a second opinion about particular financial planning milestones. Individuals here may seek a one-time consultation with an advisor as they implement their strategy. A profile score in this quadrant is associated with a “validator persona.”

Validators tend to have a high degree of longevity concerns and greater levels of loss aversion—i.e., the persistent fear of losing money, which can lead to rash decisions. Their low levels of self-efficacy may lead them to seek reassurance from a professional. To provide appropriate assistance to validators, advisors might consider expanding their services to offer financial planning as a stand-alone product, separate from asset management.

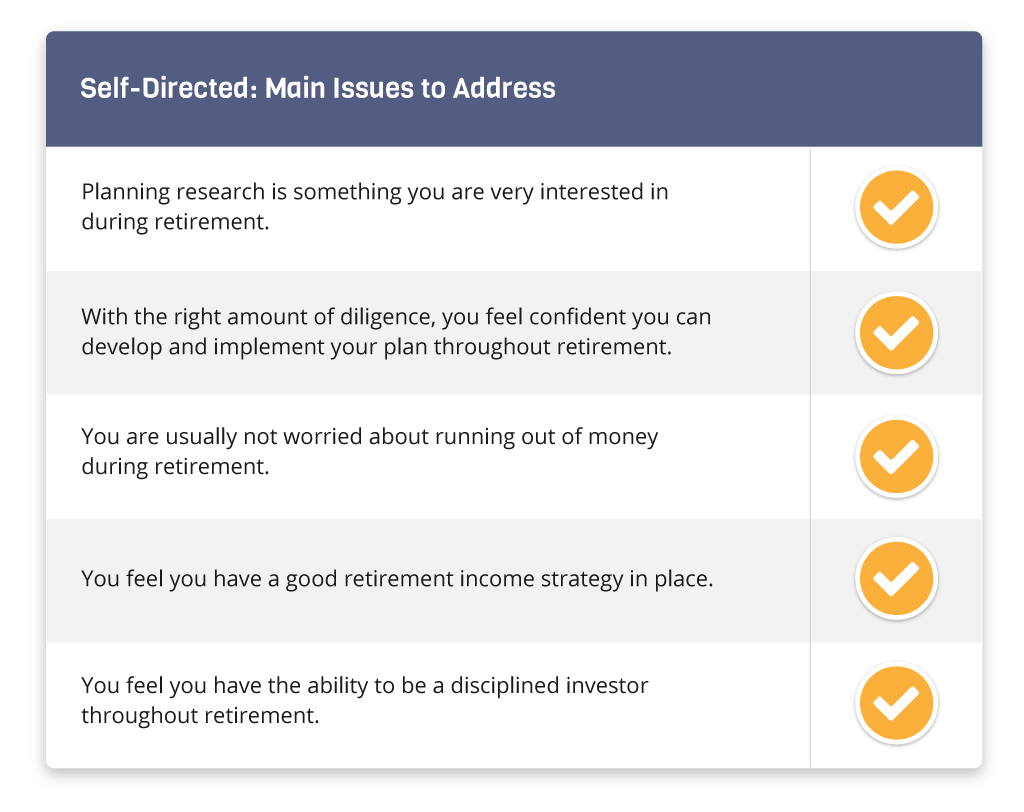

The Self-Directed Investor

The bottom right quadrant describes people who are high on financial self-efficacy but low on perceived advisor usefulness. These folks are so confident about their ability to create and implement a retirement income plan that they feel they don’t need outside help; they feel that engaging an advisor wouldn’t be worthwhile or cost effective. This quadrant reflects a “self-directed persona.”

In contrast to delegators, self-directed investors tend to exhibit low levels of longevity concern, financial biases, and inertia. While they are less likely to utilize an advisor, advisors can try a number of approaches to engage their interests and help them carry out a successful retirement income plan. For instance, it’s a good idea to give them access to unbiased educational material about the practical application of retirement income strategies. These people want to be actively involved in their retirement income planning, and they have a high degree of self-efficacy—strengths that should be leveraged. Some automated advisory applications might be suitable for this population.

Conclusions

Given these quadrants, these personas, the Financial Implementation Matrix™ is a clear, effective way to determine what approach is best suited to implementing a retirement income plan. It’s also a window onto how financial professionals might approach different types of people in or near retirement—a far better method than attempting to convince every investor willy-nilly to follow what an advisor recommends. It can be a steppingstone to learning the complexities of developing and then implementing a sound retirement income plan.

The four investor personas we’ve delineated—based on measures of advisor usefulness and retirement income self-efficacy—are based on each individual’s unique preferences for how to implement a retirement income plan. Within the personas, we have identified the specific approaches that best fit each one’s style. For retirees and near-retirees, this knowledge will help them focus on their strengths, which is essential for implementing a solid retirement income plan. For advisors, it’s a new way of understanding how best to approach certain clients and build successful, long-lasting professional relationships. Having greater, deeper insights into how well clients follow what’s presented to them, and how likely they are to stick with a strategy, can help assure adherence to a plan and, therefore, generate more successful outcomes.

For example, a delegator and a collaborator need a different cadence from their advisors. Validators and self-directed investors, on the other hand, may need options that don’t require an ongoing professional relationship. It’s a matter of identifying and managing the appropriate fit. If, say, an advisor knows a client’s financial literacy (a.k.a. numeracy) and self-awareness, the advisor can tailor investment presentations and recommendations in a more productive manner. If the advisor understands how a client might interpret the investment landscape or current events, it might be wise to reach out and discuss these issues before the client jumps to conclusions that could harm the retirement income plan. Furthermore, if you have a sense of how well a client implements advice, you can present next steps with more confidence.

Next Steps

We include the Financial Implementation Matrix in our RISA®profile process. In this process, we identify your unique retirement income style, how to match it with relevant strategies, and how best to implement your strategy. That’s because you’ll know your specific implementation strengths and weaknesses—and the best implementation avenues available that suit your persona.

So what are you waiting for? Start the process toward greater self-awareness and retirement income empowerment. Even if you already have an advisor, it can only improve the relationship. You’re sure to gain the ability to smoothly implement a more satisfying, better fitting retirement income strategy!