How the RISA® Can Help You Select the Right Retirement Income Strategy

How to Select a Retirement Income Strategy that is Right For You

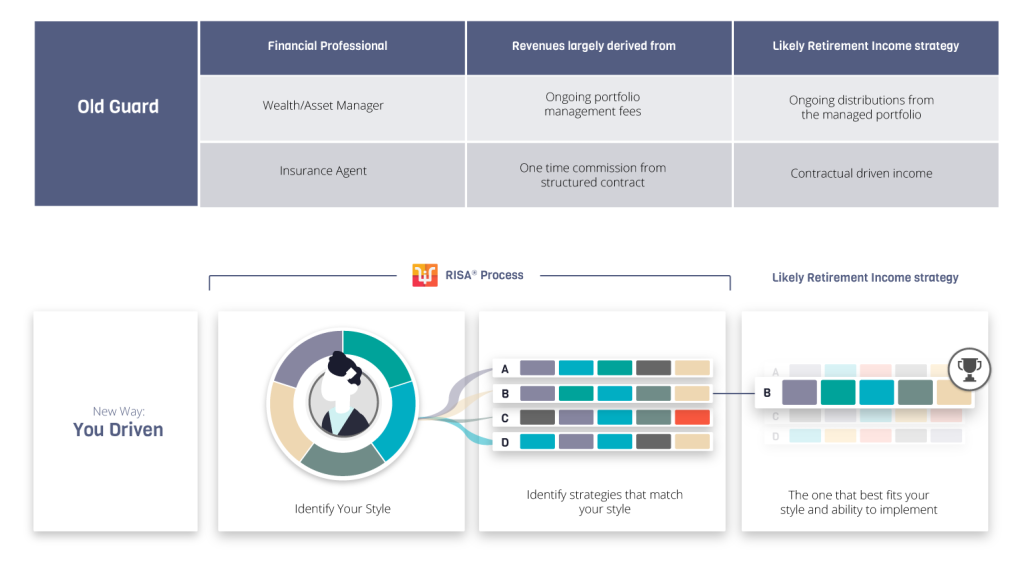

Selecting a retirement income strategy that best fits your particular preferences and lifestyle is not an easy task. While there are many credible strategies available, culling through them can be exhausting and often fruitless. You may seek expert advice, but the way recommendations have traditionally been provided is flawed. Financial advisors only know so much about you. Moreover, as honest and well-meaning as they may endeavor to be, they can’t help tending to recommend the options they feel most comfortable with or are licensed or incentivized to provide, with little consideration for how you personally prefer to source retirement income.

But our Retirement Income Style Awareness (RISA®) tool, on the other hand, identifies retirement income solutions based entirely on your unique profile. From there, you (or your advisor) can see a range of options and choose what’s best for you. Here’s a little about how it works and why it’s better.

The old way, and its flaws during retirement

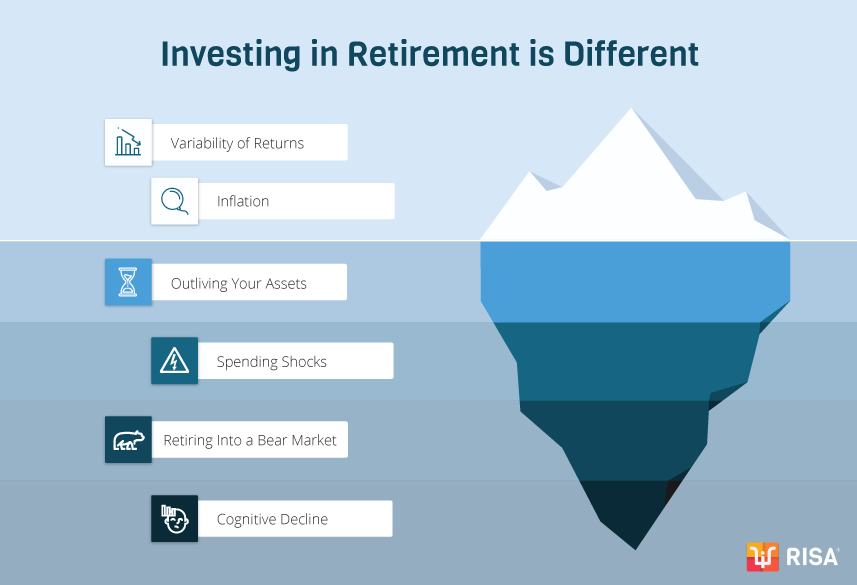

At the beginning of your financial journey, before setting up your portfolio, you may have answered a risk-tolerance questionnaire that led to a specific asset allocation mix. This probably worked well when you were still primarily concerned with accumulating wealth, but it really doesn’t address how you want to source your retirement income once you’ve moved out of the accumulation phase.

Investing for retirement is different and requires consideration for a whole new set of risks. Remember, you are no longer working and do not have the luxury of simply waiting out negative economic conditions while you are still receiving a paycheck. These new retirement risks include but are not limited to retiring into a significant market downturn, outliving your assets, declining health and cognitive abilities, and managing unexpected spending shocks.

While investigating retirement income strategies to account for these risks is attainable, their potential permutations can be exhausting to contemplate, let alone weed through. They also may be scarcely aligned with your particular preferences or personality, if at all.

Strategy-Style alignment

The way these old-school strategies are typically recommended, with little to no consideration for your unique retirement style, can lead to bad outcomes. Failing to address personal preferences typically results in strategies that aren’t properly implemented or followed. This, in turn, can lead to costly and constant revisions of your retirement plan.

For a plan to work over the long haul, a retiree must feel fully comfortable with it. It can’t just come from a financial professional or investment guru without consideration for the client’s personal tastes. Forcing the “wrong” strategy on someone is a misalignment, a disaster waiting to happen.

That’s why we created a workable model for retirement income planning that matches preferences and styles to their associated retirement income strategies.

The RISA® solution

The RISA® solves the problem of scattershot retirement planning. Through a series of user-friendly questions, it zeroes in on your unique profile to generate custom-tailored retirement income solutions. It’s designed to capture the multifaceted aspects of a retirement income plan beyond a traditional accumulation-focused portfolio that’s guided by very limited risk-tolerance questions. Instead, the RISA® measures a variety of factors related to how you’d like to source your retirement income. It then translates your preferences into a snapshot of appropriate, viable approaches that fit your personality and style.

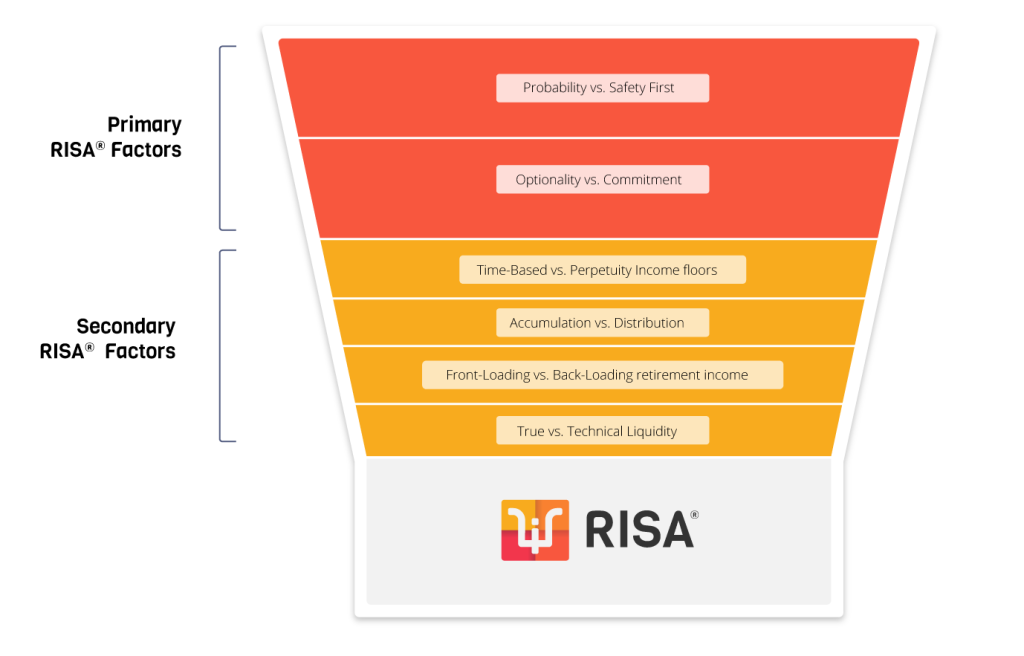

How do we do this? We’ve broken down retirement income styles into specific dimensions that gauge your preferences in relation to financial decision-making. Your RISA® Profile is derived primarily from your responses to two key scales: Probability-Based vs. Safety First (PS) and Optionality vs. Commitment (OC).

The first details exactly how you’d like to source your retirement income. Probability-Based income sources are dependent on the potential for market growth to provide a continuous and sustainable retirement income stream. Safety-First income sources incorporate contractual obligations that are less exposed to market swings and don’t depend on market growth, such as defined-benefit pensions, government bonds, or annuities with lifetime income projections.

The second measurement looks at your relative degree of flexibility. Optionality reflects a preference for keeping options open in order to respond to economic developments or changing personal situations. Commitment reflects a preference for committing to one solution, which generally means you’re less concerned about unfavorable economic or personal developments because you’re confident that your strategy solves for such possibilities.

In addition, four secondary factors provide further refinement. The Time-Based vs. Perpetuity (TP) factor refers to different income planning approaches—funding in fixed windows of time versus funding an income floor that lasts in perpetuity. Second, Accumulation vs. Distribution (AD) relates to the difference between concentrating on portfolio growth (i.e., accumulation) while retired, even though it may entail a bumpier income stream, or focusing on maintaining a more predictable income stream (distribution), even if that means not leaving the biggest amount possible at death.

Third, Front-Loading vs. Back-Loading income (FB) references the amount and pace of income you receive throughout retirement. If you expect to spend more money enjoying your early retirement years, you probably favor Front-Loading Income. But if you fear outliving your assets, you have what’s called a “longevity risk aversion,” meaning you’d prefer Back-Loading Income and being more conservative with distributions in early retirement. Lastly, True vs. Technical Liquidity (TT) is the difference between preferring to have assets earmarked as reserves for future unexpected events or to raise cash for unexpected expenses from assets that are earmarked for other purposes, as necessary.

Your RISA® Profile

Your RISA® Profile is derived from a simple but in-depth questionnaire. Expressed as a range of choices, the questionnaire examines each of these factors to measure your individual preferences. Rating a variety of real-world scenarios on a scale of 1 to 6, you help us identify the subtleties and complexities of your retirement wishes and biases.

From there, with this foundation of distinct factors to identify your preferences, we define your RISA® Matrix. The Matrix examines how scores calculated for each RISA® factor can be utilized and matched to appropriate retirement income strategies. It translates your preferences and style markers into appropriate and practical retirement income approaches. More specifically, depending on where your responses land on the two primary dimensions, the Matrix lays out four quadrants to delineate your individualized retirement income profile. It then uses the four secondary factors to fine-tune and strengthen the case for matching specific retirement income strategies to respondents who fall within each of these four quadrants. Next, from the available retirement income options, we identify the four main strategies that match up with the four RISA® Matrix quadrants.

Mapping the RISA® Matrix

Figure 1 (below) illustrates how we compile the RISA® Matrix. By aligning the Probability-Based vs. Safety First (PS) scale horizontally and the Optionality vs. Commitment (OC) scale vertically, we can separate and identify four distinct retirement income strategy quadrants.

If you land on the top-right quadrant of the RISA® Matrix, your preferences lean toward both Probability-Based and Optionality. Probability-Based and Optionality preferences identify with a Total Return approach. That means you likely prefer to draw income from a diversified investment portfolio rather than using contractual sources to fund your retirement expenses. You expect portfolio growth to support a sustainable spending rate. In addition, you don’t mind the inherent variability of drawing income from an investment that will fluctuate in value. As for secondary characteristics in this quadrant, you likely support an Accumulation focus, Technical Liquidity, Front-Loading for spending, and Time-Based income flooring.

The lower-left hand quadrant reflects individuals with a Safety-First and Commitment orientation. This reflects a protected income approach which allows for immediate and deferred annuitization to support greater downside spending protection by relying on contractually guaranteed lifetime income. Other secondary factors include having a Distribution mindset, a preference for Perpetuity income flooring, a preference for True Liquidity, and a desire to Back-Load spending to manage the fear of outliving assets. These characteristics align with retirement income strategies that provide a contractual lifetime income floor for essential or core retirement expenses, using a more diversified Total Return portfolio for discretionary expenses.

The remaining two quadrants reflect more hybrid approaches. These are better aligned with those who may not hold all the natural correlations between the different retirement income factors. Shifting to the lower-right quadrant of the RISA® Matrix, we find folks whose RISA® Profile shows both a Probability-Based and Commitment orientation. While these people are likely to maintain a Probability-Based outlook with a desire for market participation, they also have more desire to commit to a solution that provides an opportunity for a structured income stream. These preferences reflect a Risk Wrap strategy, which provides a blend of investment growth potential with lifetime income benefits, generally through a variable or fixed indexed annuity. Such tools can be designed to offer upside growth potential alongside secured lifetime spending, even if markets perform poorly. The associated market exposure satisfies the Probability-Based dimension. Purchasing a more structured and secured retirement income guardrail through the lifetime income benefit addresses the Commitment dimension and the longevity risk aversion that are present in this quadrant. From the secondary factors, this quadrant is also strongly associated with a preference for Back-Loading retirement income to better manage fears about outliving assets.

Finally, the upper left quadrant reflects another hybrid case. Those who fall in this quadrant prefer both Safety-First and Optionality. They like contractual protections but don’t like sacrificing flexibility. In addition, they tend to favor True Liquidity and Front-Loading. The desires reflected here relate to the investment-based Time Segmentation approaches, also referred to as Bucketing strategies. In this approach, you divide your money into different categories, earmarking assets for spending immediately, soon, or later. In such cases, bond ladders are often a good solution, with contractually-protected instruments (e.g., cash equivalents or government-issued securities) for shorter to intermediate income needs and a diversified investment portfolio for longer-term expenses; the longer-term portfolio can gradually replenish the short-term buckets as they are used up. Some people may also lump Time Segmentation together with the idea of holding additional cash reserves outside the investment portfolio to manage market volatility or fund unexpected expenses. These strategies address the need for asset safety by including short-term contractual protections while maintaining a high degree of optionality for other investment assets.

Does the RISA® work?

The two main RISA® factors, Probability-Based vs. Safety-First (PS) and Optionality vs. Commitment (OC), were shown to successfully identify retirement income styles and provide statistically significant predictability into how they are matched with the main retirement income strategies: Total Return, Risk Wrap, Income Protection, and Time-Segmentation. In addition, the RISA® Profile revealed how the four secondary factors further refine the predictability of respondents’ retirement income approaches. In addition, these initial retirement income strategies within the quadrants aren’t rigid recommendations, but rather starting points for analysis. For instance, while a protected income solution fits within the lower left quadrant, there are varying degrees of sensitivities that might indicate different types of protected income strategies. Our paper, “A Model Approach to Selecting a Personalized Retirement Income Strategy,” provides a detailed review of these findings.

In short, the RISA® is the first tool to capture all these aspects of a retirement income plan. It demonstrates both reliability and validity, which means you now have a multidimensional tool that does a better job of identifying retirement concerns, retirement income styles, and your preferred and most appropriate retirement income sources, than anything that’s come before. User feedback also indicates a very high degree of satisfaction with the RISA® results and strategy recommendations.

Conclusion

Discussions about retirement income planning can become confusing as there are so many different viewpoints expressed in the consumer media. Everyone must ultimately identify the style and its associated strategies that can best support her or his financial and psychological needs for retirement. You and your financial professionals should understand which styles you identify with the most, in order to know how well your preferences fit with various recommendations. It’s a way to make sense of the many competing yet viable views about how to approach retirement income planning. Understanding your retirement income style will help you navigate a framework for building the right retirement income plan for you.

The characteristics that the RISA® reveals can point you in the right direction—to a retirement income strategy that will feel comfortable and, therefore, is far more likely to succeed. This means you can quickly identify and assemble a retirement income strategy without the costly effects of trial and error.

It’s a more effective retirement income approach than arbitrarily choosing from a range of strategies based on a narrow set of parameters that scarcely consider individual retirement income styles or are drawn from a financial pundit’s subjective viewpoint. What’s more, you can be confident in the RISA® system’s predictive validity. By obtaining your RISA® Matrix, you have the empirical basis for a retirement income plan that’s based entirely on your unique leanings and particularities. This is a big step forward in retirement income planning, one that will lead to a more effective approach that achieves a feeling of “buy in” satisfaction and lays the foundation for better retirement outcomes. It places you at the forefront of the decision-making process.

While everyone should conduct a thorough financial plan to assess the economic viability of any approach, understanding your RISA® Profile will provide a valuable and validated starting point.

Next Steps

So, what are you waiting for? Go ahead and explore what strategies may be the best fit for you. Take the RISA® questionnaire and discover a range of strategies that fit who you are. Delve into your RISA® Matrix quadrants and see the retirement income strategies that match your choices. Once armed with that knowledge, you will be empowered to choose the right strategy for your retirement. No special ability or preparation is needed to start, but the self-discovery and custom-tailored retirement income strategy framework you’ll uncover will put you firmly in the driver’s seat.