A retirement income strategy based on sustainable withdrawals from an investment portfolio.

Time in the Market

Introduction

Finding and implementing the right strategy for sourcing your retirement income can be a daunting task. A myriad approaches and options are available, and truthfully, many of them will probably work all right, more or less, at least for a time. But which approach is best for you—is most precisely suited to your strengths and weaknesses, your concerns and biases and priorities, your preferences and lifestyle—may be something else altogether. A strategy that’s custom tailored not just to your requirements but to your personality is one you’ll feel good about and, consequently, one you’re most likely to implement with relative ease. It’s the one you’ll be able to stick with because it feels right—and therefore, the one that’s most likely to succeed.

RISA-In-The-Retirement-Process

Our Retirement Income Style Awareness (RISA®) tool can help you identify that solution. From your unique profile, it will show you a range of appropriate options so you can choose what’s best for you. That’s because it’s designed to capture the multifaceted aspects of a retirement income plan beyond a traditional accumulation-focused portfolio guided by a minimal risk-tolerance questionnaire.

RISA® is Different

Unlike any retirement planning tool that’s come before, the RISA® was specifically built to measure a variety of choices about how you’re most comfortable sourcing your retirement income. It translates your choices into a snapshot of appropriate, viable strategies that fit your style. It’s an empowerment tool to help you find what’s best for you. No single approach or product will work for everyone, of course. So our methodology effectively identifies your particular preferences and matches them to specific retirement income strategies and recommendations for you to choose. In this way, the RISA® solves the problem of scattershot retirement planning.

Through a series of user-friendly questions, it zeroes in on your unique profile to generate custom-tailored retirement income solutions. The secret behind the system is we’ve broken down retirement income styles into specific dimensions that gauge your preferences in relation to financial decision-making.

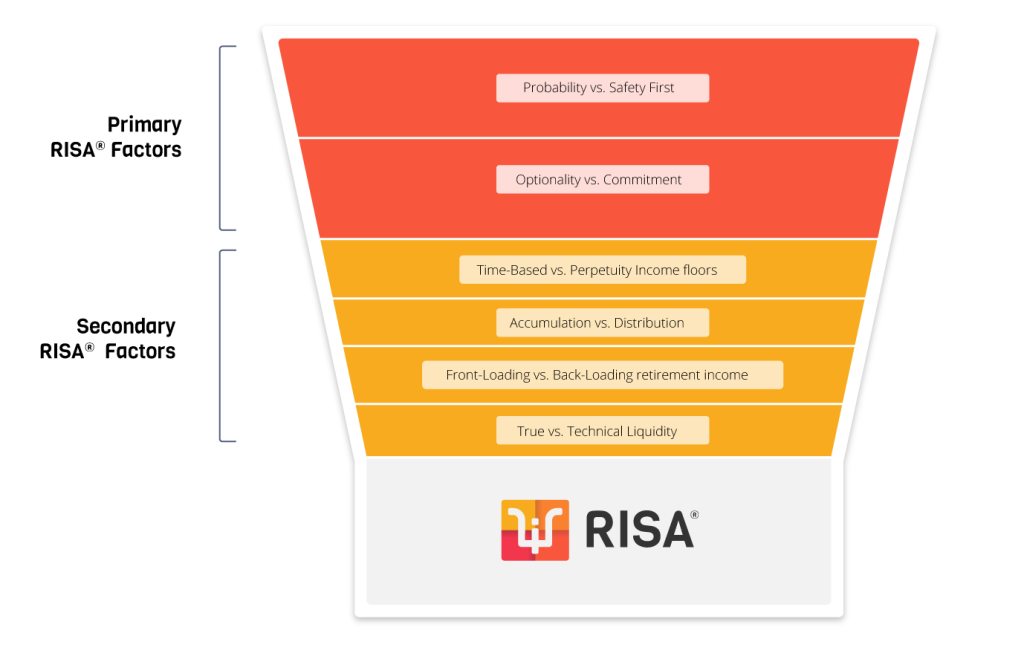

Two Primary Factors

The two primary factors our questions assess are Probability versus Safety First and Optionality versus Commitment. Probability versus Safety First details how you would like to source your retirement income—from sources dependent on potential market growth or from contractual obligations. Optionality versus Commitment delves into the degree of flexibility sought. Maybe you like to keep your options open, or your prefer to commit to one solution and be done. There are no right or wrong answers here. It’s all a matter of preference.

Four Secondary Factors

We then examine four secondary factors to sharpen and refine your profile: Accumulation versus Distribution, Technical Liquidity versus True Liquidity, Front-Loading versus Back-Loading, and Time-Based versus Perpetuity planning. These dig deeper into precisely which type of approach for sourcing retirement income feels best and most fitting for you.

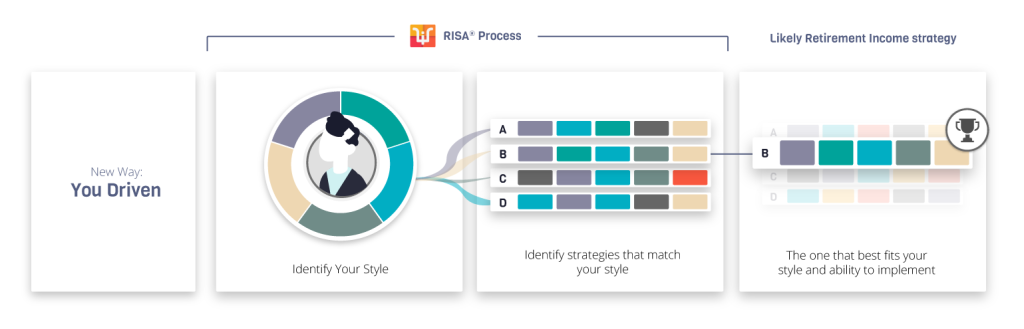

The RISA® Matrix

From there, with this foundation of distinct factors to identify your preferences, we define your RISA® Matrix, which is made up of appropriate and practical retirement income approaches. More specifically, the Matrix lays out four quadrants to delineate your individualized retirement income profile.

Next, we identify the four main strategies that match up with the four RISA® Matrix quadrants.

The Case Study

To illustrate this process, here is an example of how you can identify a retirement income approach that best fits unique personalities and preferences. Your story may be completely different. This is just sample a case study to demonstrate the effectiveness of our system. No one situation or solution is better than the others. You may or may not identify with this case, but that’s okay. What’s best for you depends entirely on who you are.

That, after all, is the point. The retirement income sourcing strategy that’s best for you is one that’s matched to your specific and unique style and preferences.

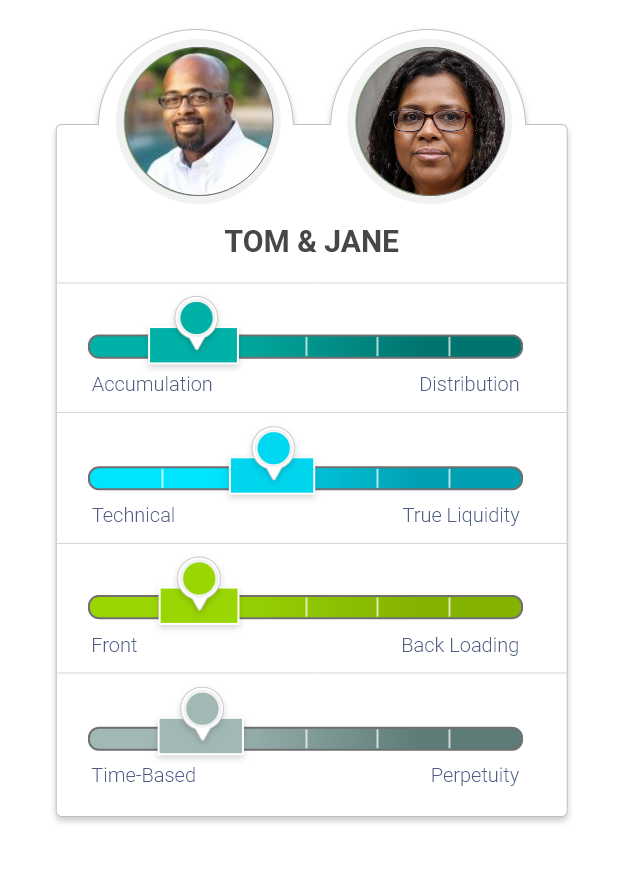

Tom and Jane

Time in the market. A retirement income strategy based on sustainable withdrawals from an investment portfolio.

Tom and Jane have been married since their early 30s. They are now approaching retirement. While successful, both have chosen a degree of autonomy in their careers. Tom, a high level company man, preferred life without high-level corporate pressures; Jane is a self-employed graphic designer. They have three adult children.

Currently, Tom wants to work five more years before retiring. While he feels comfortable with this window, he also knows that nothing is certain. His business could take a turn for the worse, thus altering his retirement schedule. Jane is less concerned about timing because she can always manage her working schedule and retirement timeline as she needs or wishes.

Throughout their careers, they’ve contributed the maximum amount allowable to their retirement accounts. While they did save for their children’s college tuitions, they always saved for retirement first. They’ve never been overly spartan about their savings; they’ve indulged in periodic discretionary expenses and favored home improvement projects. They were, however, fortunate in avoiding major spending shocks while building their asset base. In retirement, they want to be able to use their invested assets to enjoy the retirement phase of their lives, especially while they’re still young enough and healthy enough to do so. Their nest egg should be able to maintain the kind of overall spending level they want.

That’s fortunate. Over the course of their investment history, Tom and Jane were unfazed by market volatility. Their larger concern was determining an effective asset allocation and portfolio withdrawal strategy for their retirement income needs. They realize that market volatility is par for the course. So, to take a sustainable series of withdrawals from their investment portfolio, they need sustained portfolio growth. They have always kept their cash accounts to a responsible minimum because overweighting bonds or being out of the market was an expensive opportunity cost for them, relative to the perceived safety of bond funds and cash. If Tom and Jane ever needed extra cash for unforeseen expenses during their working years, they would simply raise funds from their investment portfolio. They figured they could continue doing this in retirement. They’re not particularly worried about running out of assets; they’ll make spending concessions if necessary. Still, enjoying retirement and catching up on missed traveling—especially hiking in the southwestern U.S.—are high priorities.

RISA® Interpretation

Through the RISA® questions, we were able to pull out many of the preferences that Tom and Jane exhibited before retirement.

Their RISA® profile looked like this:

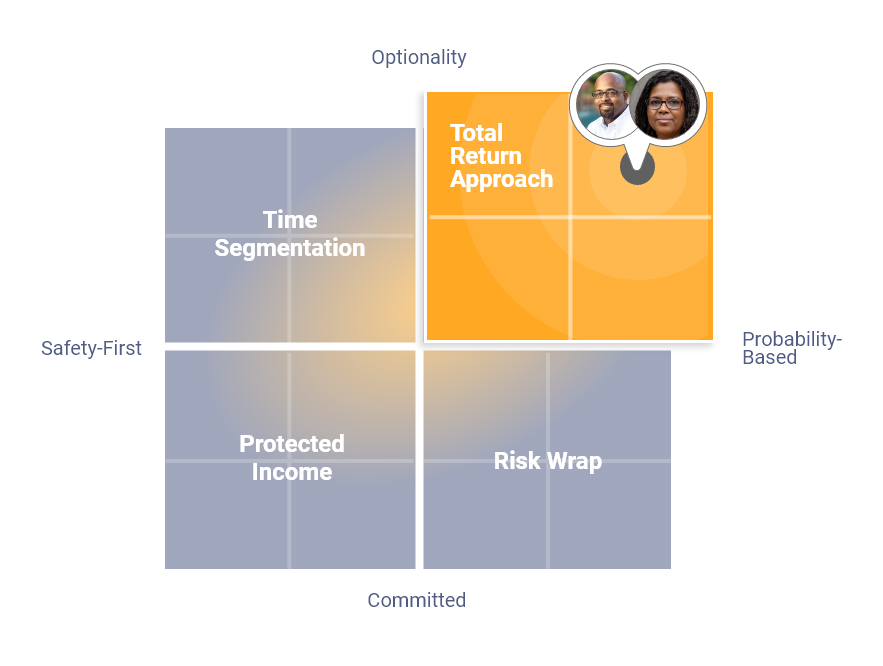

On the two primary factors, they came out like this:

From these scores, the RISA® indicated that Tom and Jane prefer to draw retirement income from a diversified investment portfolio rather than using contractual sources. They expect their investment portfolio’s growth to support a sustainable spending rate, and they don’t mind the inherent variability of drawing income from an investment that will fluctuate in value. They also enjoy the flexibility of periodically reassessing their retirement income strategy. They like to keep their options open in order to respond to economic developments or changing personal situations.

We then used the secondary factors to hone in more tightly. This is how they scored on these:

Their secondary RISA® factors exhibited a preference for increasing their asset bases rather than having a consistent and reliable income stream across different market environments. They prefer raising cash for unexpected expenses from a general investment asset base, rather than earmarking specific funds for this purpose. They favor frontloading retirement expenses so they can enjoy their retirement years while they’re still young enough and healthy enough to be active. They intend to address potential funding gaps for fixed periods of time as needed.

Tom and Jane’s RISA® score reflected many of the preferences they displayed throughout their pre-retirement accumulation years. A Total Return retirement income strategy serves as a great starting point for them. With the RISA® in hand, Tom and Jane can quickly assemble a retirement income plan focusing on the factors they care about most—a plan that suits them to a T and is likely to last.

Conclusion

While this case study may not match your situation, the RISA® is specifically designed to capture your unique set of biases, leanings, and preferences. It’s a tested and effective custom-tailored tool for an age-old problem: how to structure a retirement income sourcing strategy that feels right and will go the distance.

Financial experts are full of ideas and approaches to retirement income planning, many of which are valid. But they are not based on this kind of detailed assessment of your particular personality and financial style. Our RISA® system solves the problem of cookie-cutter methods by weighing specific measures of how you want to source your retirement income. As in the case described above, the RISA® will generate an appropriate matrix that matches suitable and available retirement income strategies to your particular quirks and desires.

Once you’re armed with this information, you will become a more informed consumer. You will be empowered to choose the right retirement income strategy for you—one that fits as comfortably as an old pair of jeans, one that will feel right for the length of your retirement. That’s important for not just your retirement satisfaction but your ability to stick with the plan. You can’t be expected to implement a strategy that just doesn’t feel right. That’s a recipe for disaster. But with the RISA® assessment, you can feel certain of finding the ideal approach for your situation and personality. That’s one you’ll be able to implement with confidence and ease. As such, it’s the retirement income sourcing plan that’s most likely to succeed for the long haul.

RISA-How-The-RISA-Works

So take our RISA® questionnaire today. It’s easy, and you might even find it fun. But the most important reason to do it now, without delay, is that it could change the course of your retirement. It could improve your odds of successfully maintaining a retirement income strategy in a way you’ll feel good about and enable you to implement it with success.